Momentum trading¶

![]()

![]()

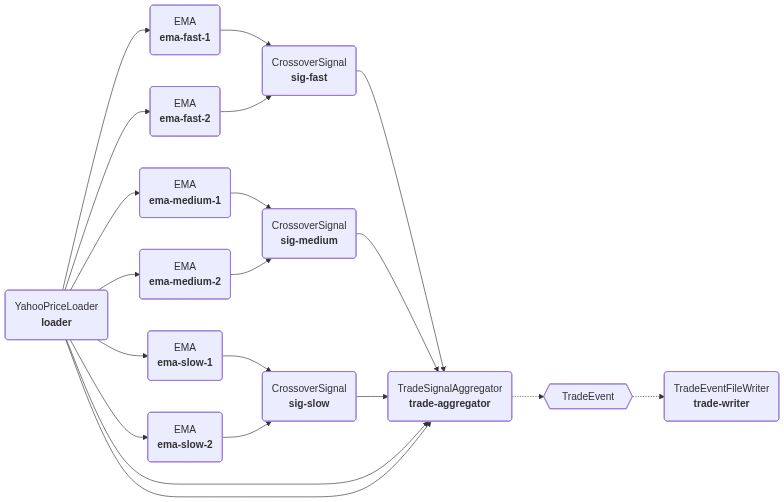

This notebook implements a simple momentum strategy on the S&P 500 using Plugboard’s event-driven components:

- Data source: streams S&P 500 prices from Yahoo! Finance;

- Indicators: three pairs of exponential moving averages (fast/medium/slow);

- Signals: compare EMAs to create buy/sell signals;

- Events: combine three signals into a TradeEvent (weak/strong buy/sell);

- Sink: write trades to a CSV file for inspection.

You can run the process, then visualize trades on a price chart.

# Install plugboard and dependencies for Google Colab

!pip install -q plugboard yfinance plotly

Here's a diagram to illustrate the whole process:

Imports and helpers¶

We import Plugboard’s core building blocks and define a small helper to create connectors:

- Components expose named inputs/outputs and can emit/receive events.

- Connectors move values between component fields.

- Event connectors route declared events between publishers and subscribers automatically.

import pandas as pd

import datetime as dt

import typing as _t

from plugboard.connector import AsyncioConnector, ConnectorBuilder

from plugboard.events import EventConnectorBuilder

from plugboard.process import LocalProcess

from plugboard.schemas import ConnectorSpec

import pandas as pd

import plotly.graph_objects as go

import yfinance as yf

from pydantic import BaseModel

from plugboard.events import Event

from plugboard.component import Component, IOController as IO

from plugboard.schemas import ComponentArgsDict

# Helper to create field connectors

connect = lambda src, tgt: AsyncioConnector(spec=ConnectorSpec(source=src, target=tgt))

Components: data and indicators¶

- YahooPriceLoader streams price and timestamp row-by-row from Yahoo Finance for ^GSPC.

- EMA consumes

priceand emits an exponentially weighted moving average asema.

Components declare their I/O via IOController, giving Plugboard enough metadata to wire processes.

def _ensure_dt(val: _t.Any) -> dt.datetime:

if isinstance(val, dt.datetime):

return val

if isinstance(val, dt.date):

return dt.datetime.combine(val, dt.time())

return pd.to_datetime(val).to_pydatetime()

class YahooPriceLoader(Component):

"""Loads historical prices for a symbol from Yahoo Finance and streams them row by row.

Outputs per step:

price: float - adjusted close price (or close if adj not present)

timestamp: datetime

"""

io = IO(outputs=["price", "timestamp"]) # stream out prices

def __init__(

self,

symbol: str = "^GSPC",

period: str | None = None,

start: str | dt.date | None = None,

end: str | dt.date | None = None,

interval: str = "1d",

limit: int | None = None,

**kwargs: _t.Unpack[ComponentArgsDict],

) -> None:

super().__init__(**kwargs)

self.symbol = symbol

self.period = period

self.start = start

self.end = end

self.interval = interval

self.limit = limit

self._data: pd.DataFrame | None = None

self._iter = 0

async def _ensure_data(self) -> None:

if self._data is not None:

return

if yf is None: # pragma: no cover - runtime safeguard

raise RuntimeError("yfinance not installed. Please 'pip install yfinance'.")

df = yf.download(

self.symbol,

period=self.period,

start=self.start,

end=self.end,

interval=self.interval,

progress=False,

)

if df.empty:

raise RuntimeError(f"No data returned for symbol {self.symbol}")

# Prefer Adj Close if exists

if "Adj Close" in df.columns:

df.rename(columns={"Adj Close": "AdjClose"}, inplace=True)

price_col = "AdjClose"

elif "Close" in df.columns:

price_col = "Close"

else:

price_col = df.columns[0]

df = df[[price_col]].rename(columns={price_col: "price"})

df.index.name = "timestamp"

df.reset_index(inplace=True)

if self.limit is not None:

df = df.head(self.limit)

# Remove column multi-index if present

self._data = df.droplevel(1, axis="columns")

@property

def df(self) -> pd.DataFrame:

"""The full DataFrame of loaded price data."""

if self._data is None:

raise RuntimeError("Data not yet loaded. Call step() first.")

return self._data

async def step(self) -> None: # noqa: D401

await self._ensure_data()

if self._iter >= len(self._data):

await self.io.close()

return

row = self._data.iloc[self._iter]

self.price = float(row["price"])

ts = row["timestamp"]

self.timestamp = _ensure_dt(ts)

self._iter += 1

class EMA(Component):

"""Computes an exponential moving average of an input price stream.

Inputs:

price: float

Outputs:

ema: float

"""

io = IO(inputs=["price"], outputs=["ema"])

def __init__(

self,

alpha: float | None = None,

span: int | None = None,

**kwargs: _t.Unpack[ComponentArgsDict],

) -> None:

super().__init__(**kwargs)

if alpha is None and span is None:

raise ValueError("Provide either alpha or span")

if alpha is not None and not (0 < alpha <= 1):

raise ValueError("alpha must be (0,1]")

self.alpha = alpha if alpha is not None else 2 / (span + 1)

self._ema: float | None = None

async def step(self) -> None:

price = float(self.price)

if self._ema is None:

self._ema = price

else:

self._ema = self.alpha * price + (1 - self.alpha) * self._ema

self.ema = self._ema

Components: signals and events¶

- CrossoverSignal reads two EMAs (

fast,slow) and emits a directionalsignal. - TradeSignalAggregator takes three signals plus the current

priceandtimestamp, and emits aTradeEventwith direction/size/strength. - TradeEventFileWriter subscribes to

TradeEventand appends a CSV row per event.

class CrossoverSignal(Component):

"""Generates buy/sell/hold signal from two moving averages.

Inputs:

fast: float

slow: float

Outputs:

signal: int (1=buy, -1=sell)

"""

io = IO(inputs=["fast", "slow"], outputs=["signal"])

def __init__(self, **kwargs: _t.Unpack[ComponentArgsDict]) -> None:

super().__init__(**kwargs)

async def step(self) -> None:

fast = float(self.fast)

slow = float(self.slow)

self.signal = 1 if fast >= slow else -1

class TradeData(BaseModel):

"""Data for a trade decision.

side: "buy" or "sell"

size: number of units

price: execution price

timestamp: event time

strength: "strong" | "weak"

count_buy: number of buy signals

count_sell: number of sell signals

"""

side: _t.Literal["buy", "sell"]

size: int

price: float

timestamp: dt.datetime

strength: _t.Literal["strong", "weak"]

count_buy: int

count_sell: int

class TradeEvent(Event):

"""Event emitted when strategy decides to trade."""

type: _t.ClassVar[str] = "trade_event"

data: TradeData

class TradeSignalAggregator(Component):

"""Aggregates three crossover signals into trade events.

Inputs:

s1, s2, s3 (int signals: 1 buy, -1 sell, 0 hold)

price (float)

timestamp (datetime)

Output events:

TradeEvent

Logic:

strong buy = 3 buys -> size 2

weak buy = 2 buys 1 sell -> size 1

strong sell = 3 sells -> size 2

weak sell = 2 sells 1 buy -> size 1

"""

io = IO(

inputs=["s1", "s2", "s3", "price", "timestamp"],

output_events=[TradeEvent],

)

def __init__(self, **kwargs: _t.Unpack[ComponentArgsDict]) -> None:

super().__init__(**kwargs)

self._previous_signal: int | None = None

async def step(self) -> None:

signals = [int(self.s1), int(self.s2), int(self.s3)]

count_buy = sum(1 for s in signals if s == 1)

count_sell = sum(1 for s in signals if s == -1)

net_signal = count_buy - count_sell

if net_signal >= 2:

decision, strength, size = "buy", "strong", 2

elif net_signal == 1:

decision, strength, size = "buy", "weak", 1

elif net_signal <= -2:

decision, strength, size = "sell", "strong", 2

elif net_signal == -1:

decision, strength, size = "sell", "weak", 1

if net_signal != self._previous_signal:

self._logger.info(

f"Emitting trade decision", decision=decision, size=size, strength=strength

)

trade = TradeEvent(

source=self.name,

data=TradeData(

side=decision,

size=size,

price=float(self.price),

timestamp=_ensure_dt(self.timestamp),

strength=strength,

count_buy=count_buy,

count_sell=count_sell,

),

)

self.io.queue_event(trade)

self._previous_signal = net_signal

class TradeEventFileWriter(Component):

"""Consumes trade events and writes them to a CSV file (append mode)."""

io = IO(input_events=[TradeEvent])

def __init__(self, path: str = "trades.csv", **kwargs: _t.Unpack[ComponentArgsDict]) -> None:

super().__init__(**kwargs)

self.path = path

# Write header

with open(self.path, "w", encoding="utf-8") as f:

f.write("timestamp,side,size,price,strength,count_buy,count_sell,source\n")

@TradeEvent.handler

async def handle_trade(self, event: TradeEvent) -> None: # noqa: D401

d = event.data

with open(self.path, "a", encoding="utf-8") as f:

f.write(

f"{d.timestamp.isoformat()},{d.side},{d.size},{d.price:.4f},{d.strength},{d.count_buy},{d.count_sell},{event.source}\n"

)

Wire the process¶

Here we:

- Instantiate the source, indicator, signal, aggregator, and writer components.

- Connect fields with

AsyncioConnector(price→EMAs, EMAs→signals, signals→aggregator). - Build event connectors so

TradeEventflows from the aggregator to the file writer. - Create a

LocalProcessto run everything in-process.

# Build components

price_loader = YahooPriceLoader(name="loader", period="10y", interval="1d")

# Three EMAs with different speeds (adjust spans as desired)

ema_fast_1 = EMA(name="ema-fast-1", span=8)

ema_fast_2 = EMA(name="ema-fast-2", span=15)

ema_medium_1 = EMA(name="ema-medium-1", span=30)

ema_medium_2 = EMA(name="ema-medium-2", span=50)

ema_slow_1 = EMA(name="ema-slow-1", span=80)

ema_slow_2 = EMA(name="ema-slow-2", span=150)

# Signals from different pairings

sig_fast = CrossoverSignal(name="sig-fast")

sig_medium = CrossoverSignal(name="sig-medium")

sig_slow = CrossoverSignal(name="sig-slow")

# Aggregator producing trade events

aggregator = TradeSignalAggregator(name="trade-aggregator")

trade_writer = TradeEventFileWriter(name="trade-writer", path="trades.csv")

components = [

price_loader,

ema_fast_1,

ema_fast_2,

ema_medium_1,

ema_medium_2,

ema_slow_1,

ema_slow_2,

sig_fast,

sig_medium,

sig_slow,

aggregator,

trade_writer,

]

# Field connectors

connectors = [

# Price to EMAs

connect("loader.price", "ema-fast-1.price"),

connect("loader.price", "ema-fast-2.price"),

connect("loader.price", "ema-medium-1.price"),

connect("loader.price", "ema-medium-2.price"),

connect("loader.price", "ema-slow-1.price"),

connect("loader.price", "ema-slow-2.price"),

# Convert the three pairs of EMAs into signals

connect("ema-fast-1.ema", "sig-fast.fast"),

connect("ema-fast-2.ema", "sig-fast.slow"),

connect("ema-medium-1.ema", "sig-medium.fast"),

connect("ema-medium-2.ema", "sig-medium.slow"),

connect("ema-slow-1.ema", "sig-slow.fast"),

connect("ema-slow-2.ema", "sig-slow.slow"),

# Signals + price + timestamp into aggregator

connect("sig-fast.signal", "trade-aggregator.s1"),

connect("sig-medium.signal", "trade-aggregator.s2"),

connect("sig-slow.signal", "trade-aggregator.s3"),

connect("loader.price", "trade-aggregator.price"),

connect("loader.timestamp", "trade-aggregator.timestamp"),

]

# Event connectors

builder = ConnectorBuilder(connector_cls=AsyncioConnector)

event_builder = EventConnectorBuilder(connector_builder=builder)

event_connectors = list(event_builder.build(components).values())

process = LocalProcess(components=components, connectors=connectors + event_connectors)

Run the process¶

Running the process iterates over the price history, updates indicators, produces signals, emits trade events, and writes them to trades.csv.

async with process:

await process.run()

Visualize trades from CSV¶

After the run, trades.csv contains one row per TradeEvent. We overlay buy/sell markers on the price series to see where the strategy acted.

df_prices = price_loader.df

df_trades = pd.read_csv("trades.csv", parse_dates=["timestamp"])

traces = [

go.Scatter(x=df_prices["timestamp"], y=df_prices["price"], mode="lines", name="Price"),

go.Scatter(

x=df_trades[df_trades["side"] == "buy"]["timestamp"],

y=df_trades[df_trades["side"] == "buy"]["price"],

mode="markers",

name="Buy",

marker=dict(

color="green",

symbol="triangle-up",

size=df_trades[df_trades["side"] == "buy"]["strength"].map(

lambda x: 18 if x == "strong" else 12

),

),

),

go.Scatter(

x=df_trades[df_trades["side"] == "sell"]["timestamp"],

y=df_trades[df_trades["side"] == "sell"]["price"],

mode="markers",

name="Sell",

marker=dict(

color="red",

symbol="triangle-down",

size=df_trades[df_trades["side"] == "sell"]["strength"].map(

lambda x: 18 if x == "strong" else 12

),

),

),

]

fig = go.Figure(data=traces)

fig

Visualize the process diagram¶

We can render a Mermaid diagram of the Plugboard process, showing components, fields, and event flows. This helps debug and document the model wiring.

# Visualise the process

from plugboard.diagram import MermaidDiagram

diagram_md = MermaidDiagram.from_process(process)

diagram_md.url

Next steps¶

Potential enhancements to this example could include:

- Adding a component to track PnL from the trades;

- Using

plugboard.tuneto choose the moving averages to optimise PnL.